How do high-yield savings accounts work?

Our goal here at Credible Operations, Inc., NMLS Number 1681276, referred to as "Credible" below, is to give you the tools and confidence you need to improve your finances. Although we do promote products from our partner lenders, all opinions are our own.

High-yield savings accounts offer higher interest rates than traditional savings accounts. (iStock)

High-yield savings accounts can be a great option if you’re trying to save money — no matter what your financial goals are.

A high-yield savings account works much the same as a traditional savings account, but the annual percentage yield, or APY, may be 10 times higher or more.

If you have some money you’re ready to save and are wondering where to park it, learn more about high-yield savings accounts, the benefits of opening one and factors to consider when choosing an account.

What’s a high-yield savings account?

A savings account is a type of account offered by banks and credit unions. The financial institution allows you to deposit money into the account and, in return, pays you interest on your balance.

A high-yield savings account is similar to a regular savings account, but the interest rate and accompanying APY are higher.

Because high-yield savings accounts are typically FDIC-insured, they can be a good place to keep an emergency fund or save for other short-term goals without the risk of investing in the stock market.

With Credible, you can easily compare high-yield savings rates.

How do high-yield savings accounts work?

Interest earnings on traditional savings accounts have been below 1% for more than a decade. But over the same time frame, online banks began trying to attract dollars to their vaults by offering high-yield savings accounts.

Online-only banks can afford to pay higher interest rates because they have less overhead than brick-and-mortar banks. And the higher rates can mean higher returns for customers.

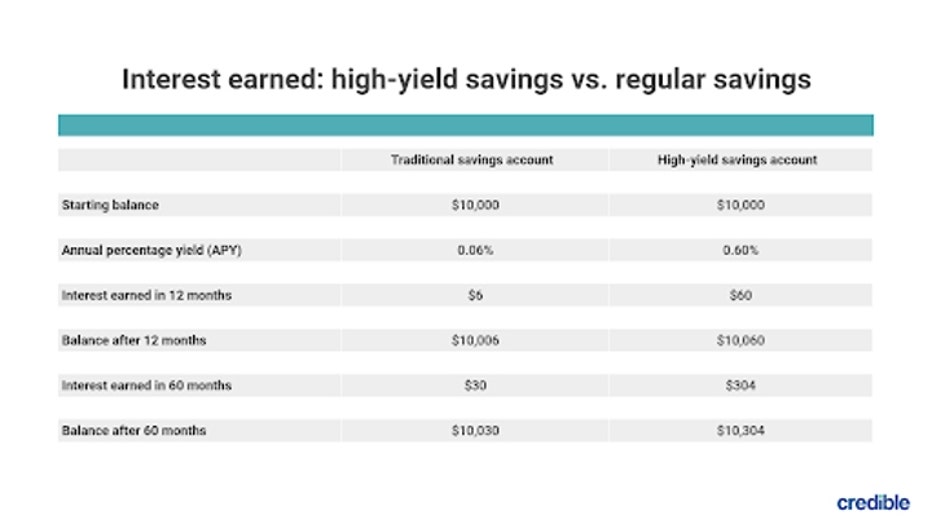

Let’s consider an example of how much more a saver might earn with a high-yield savings account.

The national average savings account rate was 0.06% as of September 2021, according to the FDIC. So let’s say you could receive an APY of 0.60% with a high-yield savings account. If you were to deposit $10,000 in each account, here’s how much you’d have in the account after one year and five years (assuming the rate stays the same, you don’t make any additional deposits and interest compounds monthly):

After five years, that’s $274 more in your account if you choose a bank that pays a higher rate. That rate of return might not be life-changing, but it illustrates the difference between traditional and high-yield savings accounts. The higher APY you can get and the more you deposit, the more your money can grow.

Online banks vs. traditional banks

The primary difference between online banks and traditional banks is that online banks offer only mobile and online access — you can’t visit a branch or meet with a banker face-to-face.

It’s that difference that allows online banks to offer higher interest rates. Online banks don’t have to pay to maintain a large network of physical branches, and they can pass those savings on to their customers.

Many traditional banks have started offering high-yield savings account options to hold on to their current customers and attract new ones. Still, you’re more likely to get the highest rates from online-only banks.

Plus, you don’t have to worry about not having access to your money. If you have an account at a traditional bank and an online account, you can still move money between accounts via electronic transfer. The transfer might not be instantaneous as it would be if both accounts were with the same bank, but your transfer should be complete within a few business days.

What are the benefits of a high-yield savings account?

If you’re wondering whether opening a high-yield savings account makes sense for you, it helps to consider the benefits.

- Higher rates — As the name implies, high-yield savings accounts tend to offer higher APYs than traditional savings accounts.

- Low or no fees — Some banks charge monthly fees, but many high-yield savings accounts have no monthly fees and low minimum balance requirements. Be sure to read the fine print before opening an account.

- Easy transfers — Online banks usually make it easy to transfer money between your high-yield account and outside accounts via their website, mobile app or by calling customer service.

- Security — Banks that offer high-yield savings accounts are typically FDIC-insured, just like traditional bank accounts, so you don’t have to worry about losing your savings if the financial institution goes under.

You can compare high-yield savings account rates from various financial institutions in minutes using Credible.

Best uses for a high-yield savings account

Different types of accounts serve different purposes, and many people have separate accounts for paying daily expenses, saving for an emergency and other short-term needs and saving for retirement. Here are some of the best uses for a high-yield savings account:

- Emergency fund — Having an emergency fund is essential to your financial well-being. Storing extra cash in a high-yield savings account ensures you have money available to cover bills if you lose your job, face a medical emergency or another unexpected expense. Your savings will grow faster in a high-interest account than a traditional savings account, but you can still access the money if you need it.

- Short-term savings — High-yield savings accounts are a great way to save for short-term goals, like a new car or a vacation.

- Longer-term savings — A high-yield savings account can also be a great way to save for longer-term goals, like buying a home, because you’ll earn more with compound interest.

Despite their versatility, high-yield savings accounts aren’t a good fit for retirement savings. Even high-interest savings accounts offer a relatively low rate of return compared to investment accounts like a 401(k), traditional IRA or Roth IRA. Plus, interest earned in a high-yield savings account is taxable, whereas investment earnings in a qualified retirement account are tax-deferred (or tax-free in the case of a Roth IRA). These tax benefits allow you to save even more for retirement.

HOW TO CHOOSE A HIGH-YIELD SAVINGS ACCOUNT

What to look for in a high-yield savings account

Like any other financial product, rates, features and benefits of high-yield savings accounts vary from bank to bank. For that reason, it’s a good idea to shop around and compare multiple account options.

Consider these six factors in your selection process:

- Initial deposit requirements — Some financial institutions have minimum deposit requirements for opening an account, although not all do. Consider how much money you have available to open the account to make sure you can meet any minimum.

- Annual percentage yield (APY) — To get the greatest return on your savings, you want to find the highest APY possible. Just be sure to read the fine print. Some banks offer high introductory rates to get customers to open accounts, then lower the rate after a few months.

- Minimum balance requirements — Some banks require you to keep a minimum balance in your account to earn the stated return or avoid fees.

- Low fees — Fees can chip away at your returns, so check whether the account you plan on opening charges a monthly maintenance fee, minimum balance fee or any other type of fee.

- Deposit and withdrawal options — Regulation D is a federal banking rule that impacts how your bank or credit union manages your deposits — including those made into high-yield savings accounts. Part of Regulation D restricted how often customers can move money out of their savings and money market accounts to six withdrawals per month. In April 2020, the Federal Reserve lifted that limitation, permitting financial institutions to allow their customers to make more than six payments or withdrawals from their accounts. But banks and credit unions aren’t required to make this change. Your financial institution may maintain its old withdrawal rules, charge fees when you exceed six payments or withdrawals per month and even close your account if you regularly exceed the limit.

- Customer service — If you have questions about your account, it’s important to be able to get help when you need it. So consider the financial institution’s customer support options. For example, is support available by phone, email or live chat? Is it available 24/7, or only during business hours?

How do I get a high-yield savings account?

If you’re interested in getting a high-yield savings account, opening one is usually pretty easy.

- Shop around and compare accounts. Using the criteria outlined above, choose an account that best fits your needs and offers a competitive APY.

- Apply. The exact application process varies from bank to bank, but it’s similar to opening any other type of savings account. You’ll need to provide basic information, such as your name, Social Security number, address and phone number. Many financial institutions also require new customers to provide government-issued photo identification, such as a passport or driver’s license.

- Put money in your new account. If the bank has a minimum initial deposit requirement, you may need to provide the routing and account number for the bank account you plan to transfer your initial deposit from. Some institutions will allow you to mail a check or schedule a wire transfer.

If you’re ready to find a high-yield savings account that works for you, use Credible to compare rates.

Are high-yield savings accounts safe?

High-yield savings accounts are a safe place to park your money. FDIC insurance covers checking, savings and other deposit accounts up to $250,000 at banks, and the National Credit Union Administration provides similar coverage for accounts at credit unions.

Both of these institutions protect against the loss of your money in the event an FDIC- or NCUA-insured financial institution fails. So before opening a high-yield savings account, check to ensure the institution is a member of the FDIC or NCUA. You don’t need to apply for the coverage — it’s automatic when you open the account.

How often do high-yield savings rates change?

The downside of opening a high-yield savings account is that the rate you get when you open the account isn’t set in stone. The APY on a high-yield savings account is typically variable, meaning it can change at any time without notice.

Rates are tied to the federal funds rate, which is set by the Federal Open Market Committee (FOMC) — a branch of the Federal Reserve. When the FOMC raises or lowers the federal funds rate, financial institutions typically raise or lower interest rates on deposit accounts as well.

And while the Truth in Savings Act requires financial institutions to notify customers of some changes to their accounts, they’re not required to notify customers of changes in the interest rate on variable-rate accounts. Instead, you’ll probably notice it after the fact, when you receive a statement or review your account online and notice that your rate’s been adjusted.

LEARN ABOUT BEST WAYS TO SAVE WHEN INTEREST RATES ARE LOW

High-yield savings accounts vs. CDs and money market accounts

Traditional and high-yield savings accounts aren’t your only savings options. Let’s consider a couple of common alternatives.

Certificates of Deposit (CDs)

A CD is a type of account offered by banks and other financial institutions that allows you to earn a fixed interest rate that’s usually higher than the rates offered by high-yield savings accounts. In exchange for that higher rate, you agree not to withdraw your money for a set period — usually anywhere from one month to five years.

If you withdraw funds before the maturity date, the bank keeps a portion of your deposit as a penalty. The longer the CD’s term, the higher the rate you’ll receive. This makes CDs a good option for short-term savings when you know you won’t need to access the funds.

Money market accounts

Money market accounts are essentially a hybrid between a checking account and a savings account. Like high-yield savings accounts, they tend to offer higher rates than traditional savings accounts. But they also allow you to write a limited number of checks or make a few debit card purchases from the account each month. Those check-writing and debit card privileges can make them convenient, but they usually require larger minimum deposits and average daily balances, meaning they’re not the right choice for everyone.